It’s Cheaper for Me to Rent! Is It?

By: Bernice Ross

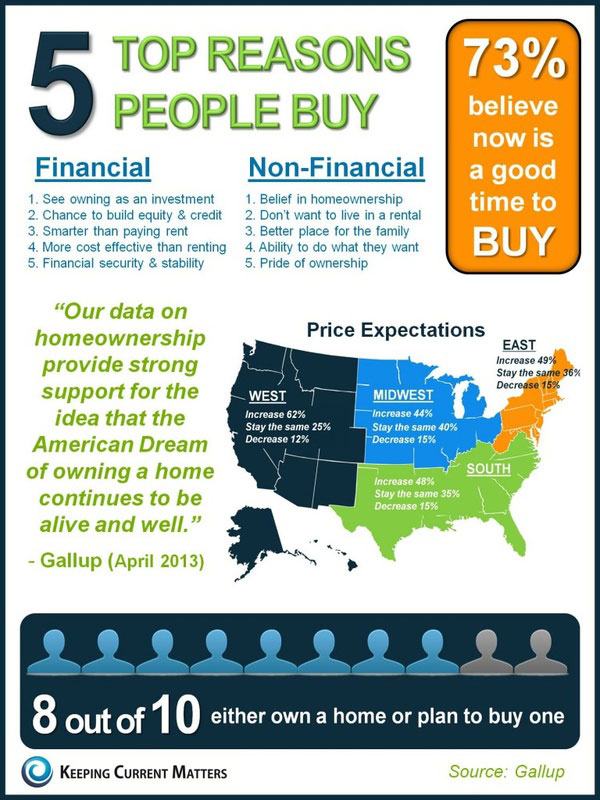

Americans believe in the dream of homeownership. With all the foreclosures and bankruptcies taking place, however, is it cheaper for people to rent rather than buying?

When it comes to the decision of renting vs. buying, most people make the decision based upon a comparison of monthly payments. If their rent payment is less than the payment on a home, many decide that it’s cheaper to rent than it is to buy. This approach, however, fails to take into account a number of other factors that influence the total costs of homeownership rather than just the monthly payments.

The first step for any person who is considering buying or selling a home is to talk to a tax professional. Each person’s tax situation is different. For example, when you purchase a primary residence, you can normally reduce your withholding taxes. The reason for this is that the interest on your mortgage is tax deductible. When you first purchase your home, almost all your monthly payment will go to interest. If you are in the 25 percent tax bracket, that means that Uncle Sam is essentially paying 25 percent of the interest on your home. This means that if you’re currently paying $1,000 per month in rent, you could afford approximately $1,250 in mortgage payments due to the tax breaks. Again, check with a tax professional to see how this applies to your situation. (There are some exceptions if you fall under the Alternative Minimum Tax law that may limit home mortgage deductions).

One of the most compelling reasons to buy rather than rent is to lock in a permanent monthly payment at today’s rates for the next 30 years. If possible, obtain a fixed rate mortgage for 30 years. This means that your mortgage 20 years from now will be at the same rate as it is today. In contrast, rent payments almost always keep pace with inflation. That payment you had to stretch to make today will be miniscule compared to payments 15 or 20 years from now.

To illustrate this point, the current 10-year average inflation rate is 2.82 percent per year. http://www.usinflationcalculator.com/inflation/current-inflation-rates/ (The average since 1913 is actually 3.41 percent a year http://www.inflationdata.com/Inflation/Inflation/AnnualInflation.asp). Assume that the inflation rate continues to average 2.82 percent per year. In 2019, your $1,000 mortgage payment would be the equivalent of $718 in today’s dollars. If your property value keeps pace with inflation, it would have increased in value by approximately 28 percent as well, making it worth $128,000. Furthermore, you would have paid down your loan for ten years. Assuming a six percent interest rate on a 30-year fully amortized fixed rate loan, your balance on your original $100,000 loan would be $83,686. Consequently, your equity position after 10 years would be $16,314 ($100,000-$83,686) plus $28,000 in appreciation due to inflation for a total of $44,314. (This calculation does not take into consideration any amount that you would have placed on the property as a down payment. That amount would be added to the $44,314).

Now compare this situation to what would happen if you were renting. If your rent payments kept pace with the inflation of 2.82 percent per year, your rent payments would increase 28.2 percent ($1,282 per month vs. $1,000 today).

Assuming a 2.82 percent inflation rate over the next 20 years, this example becomes even more compelling. Your monthly payment of $1,000 would be the same as $436 in today’s dollars. If your property value kept pace with inflation, it would now be worth approximately $156,000. After 20 years, the balance on your $100,000 fixed rate loan would be $54,359. Thus, your equity position would be $56,000 due to the inflation-related appreciation increase plus $45,641 in principal reduction for a total equity position of $101,641.

In terms of rent 20 years from now, if it kept place with inflation, you would be paying $1,564 per month. That’s an extra $6,768 per year more than if you had locked in your 30-year fixed rate loan at time of purchase.

The wild card in this entire discussion is the inflation rate. Many experts are predicting that the only way the government can pay the country’s debts is to print more money. The result will be increased inflation. Using the ten-year example from above, paying off a $1 billion dollar loan after 10 years of inflation at 2.82 percent means that the real payoff amount is $718 million in today’s dollars.

For an individual, this may be the best reason to purchase real estate. In most places, real estate is one of the few investments that keeps pace with inflation. Owning a home lets you build wealth by paying down your mortgage. If you hold your property for the long-term, it will normally keep pace with inflation creating additional wealth. When you rent, you pay off your landlord’s mortgage and make him wealthy. The choice seems obvious—build your wealth someone else’s.

When it comes to the decision of renting vs. buying, most people make the decision based upon a comparison of monthly payments. If their rent payment is less than the payment on a home, many decide that it’s cheaper to rent than it is to buy. This approach, however, fails to take into account a number of other factors that influence the total costs of homeownership rather than just the monthly payments.

The first step for any person who is considering buying or selling a home is to talk to a tax professional. Each person’s tax situation is different. For example, when you purchase a primary residence, you can normally reduce your withholding taxes. The reason for this is that the interest on your mortgage is tax deductible. When you first purchase your home, almost all your monthly payment will go to interest. If you are in the 25 percent tax bracket, that means that Uncle Sam is essentially paying 25 percent of the interest on your home. This means that if you’re currently paying $1,000 per month in rent, you could afford approximately $1,250 in mortgage payments due to the tax breaks. Again, check with a tax professional to see how this applies to your situation. (There are some exceptions if you fall under the Alternative Minimum Tax law that may limit home mortgage deductions).

One of the most compelling reasons to buy rather than rent is to lock in a permanent monthly payment at today’s rates for the next 30 years. If possible, obtain a fixed rate mortgage for 30 years. This means that your mortgage 20 years from now will be at the same rate as it is today. In contrast, rent payments almost always keep pace with inflation. That payment you had to stretch to make today will be miniscule compared to payments 15 or 20 years from now.

To illustrate this point, the current 10-year average inflation rate is 2.82 percent per year. http://www.usinflationcalculator.com/inflation/current-inflation-rates/ (The average since 1913 is actually 3.41 percent a year http://www.inflationdata.com/Inflation/Inflation/AnnualInflation.asp). Assume that the inflation rate continues to average 2.82 percent per year. In 2019, your $1,000 mortgage payment would be the equivalent of $718 in today’s dollars. If your property value keeps pace with inflation, it would have increased in value by approximately 28 percent as well, making it worth $128,000. Furthermore, you would have paid down your loan for ten years. Assuming a six percent interest rate on a 30-year fully amortized fixed rate loan, your balance on your original $100,000 loan would be $83,686. Consequently, your equity position after 10 years would be $16,314 ($100,000-$83,686) plus $28,000 in appreciation due to inflation for a total of $44,314. (This calculation does not take into consideration any amount that you would have placed on the property as a down payment. That amount would be added to the $44,314).

Now compare this situation to what would happen if you were renting. If your rent payments kept pace with the inflation of 2.82 percent per year, your rent payments would increase 28.2 percent ($1,282 per month vs. $1,000 today).

Assuming a 2.82 percent inflation rate over the next 20 years, this example becomes even more compelling. Your monthly payment of $1,000 would be the same as $436 in today’s dollars. If your property value kept pace with inflation, it would now be worth approximately $156,000. After 20 years, the balance on your $100,000 fixed rate loan would be $54,359. Thus, your equity position would be $56,000 due to the inflation-related appreciation increase plus $45,641 in principal reduction for a total equity position of $101,641.

In terms of rent 20 years from now, if it kept place with inflation, you would be paying $1,564 per month. That’s an extra $6,768 per year more than if you had locked in your 30-year fixed rate loan at time of purchase.

The wild card in this entire discussion is the inflation rate. Many experts are predicting that the only way the government can pay the country’s debts is to print more money. The result will be increased inflation. Using the ten-year example from above, paying off a $1 billion dollar loan after 10 years of inflation at 2.82 percent means that the real payoff amount is $718 million in today’s dollars.

For an individual, this may be the best reason to purchase real estate. In most places, real estate is one of the few investments that keeps pace with inflation. Owning a home lets you build wealth by paying down your mortgage. If you hold your property for the long-term, it will normally keep pace with inflation creating additional wealth. When you rent, you pay off your landlord’s mortgage and make him wealthy. The choice seems obvious—build your wealth someone else’s.

Buyer Advice: First-Time Buyers—Don’t Wait—Buy Now!

By: Bernice Ross

|

If you are a first time buyer who has been trying to decide whether to buy your first home or not, it’s time to buy now. If you miss this great opportunity, you may regret it for the rest of your life.

The Lowest Interest Rates since the 1950’s Interest rates are close to all time lows, hovering in the mid-five percent range. When I started in the real estate business in 1978, interest rates were 9 ¾ percent and soon hit 10 percent. In the downturn in the 1980s, they jumped as high as 21 percent. In the early 1990’s, they were at 12 percent. If you’re waiting because you think prices may drop more, don’t. With the government running huge deficits, they will have to sell treasury bills to cover the debt. Investors are feeling skittish about purchasing these securities. This means the government will have to increase the rate of return in order to get more investors to purchase. When the government increases these rates, the cost of home mortgages increases along with them. But Prices May Go Down! One of the concerns almost all first-time buyers have is, “Will the price go down further?” To put this in perspective, an interest rate increase of one percent on a $200,000 loan will cost you approximately $50,000 more in interest over the life of the loan. A two percent interest rate increase, which many experts believe is possible in the next 12 to 24 months, will cost you approximately $100,000 in additional interest over the life of a 30-year loan. That’s a whopping 50 percent of the loan amount. If you believe prices will go down, the question is by how much? If you believe there is another 25 to 50 percent depreciation in your marketplace, then you can run the risk of waiting. What you need to know, however, is that virtually all real estate experts are saying that we are at or very near the bottom. Proof that prices are bottoming is coming from a wide variety of places. Many of the hardest hit areas are beginning to make a comeback. Sales in California are up by 20 percent. Two major condominium buildings in Miami sold out in just six weeks. While these examples don’t represent a complete turnaround, they are concrete signs that the market is bottoming right now or may be starting to improve. In terms of how market cycles work, the excess inventory must be sold off prior to the market stabilizing in terms of price. This appears to be what is happening in many areas. Once the excess inventory disappears, you will have more competition for a limited amount of supply. This is how the next upturn in the market will begin. In fact, many first time buyers in Orange County, California are bumping into multiple offers on the homes they want. Multiple offers on first-time buyer properties are one of the sure signs that the market is improving.

We specialize in helping renters become homeowners.

|

It’s Cheaper for Me to Rent!

Assume that you are currently paying $1,500 per month rent. You would like to buy a $300,000 property with $30,000 down and a $270,000 loan for 30 years at 6¼ percent. You are in the 28 percent tax bracket and will own the property for 8 years. Appreciation only keeps pace with inflation at 2.54 percent per year. The estimated cost of renting is $142,015 vs. the estimated cost of buying which is $117,754. You save $24,261 by purchasing rather than renting. (You can use any of the online rent vs. buy calculators to make this determination for your situation.) Another challenge with renting is that you are paying off your landlord’s mortgage, not your own. Even if your house doesn’t increase in value, each month you make a payment, you accumulate wealth by paying down the principle. This is the equivalent of putting money in the bank each month. In contrast, renters lose additional wealth as their rental payments increase over time. Homeowners with a fixed rate loan have locked in their mortgage amount for the next 30 years. If there is inflation, the homeowners pay off their loan with inflated dollars. Rents, in contrast, keep pace with inflation. Thus, if you elect to wait to purchase, you may be leaving money on the table in two different ways. First, if the interest rates increase, you will end up paying more over the term of their loan. Second, by waiting to take action, you will accumulate less wealth and experience less appreciation. Furthermore, the longer you wait to start paying down a mortgage, the later the date will be that you retire that debt. |

|

|